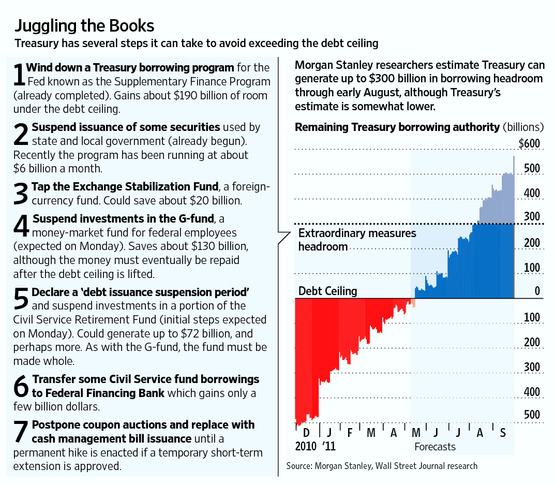

On Oct 19th Reuters released an article title: “Is Bank of America preparing for a Chapter 11.” This story circulated the financial press like wild fire and although the author Christopher Whalen related some the of recent facts on how BOA had to foot over a $10 billion plus legal settlement and the recent decision of charging some customers $5 per month for using their debt card which in his opinion spurred the Occupy Wall Street movement. He does point out a recent administrative move of the bank moving all of the derivatives from Merrill Lynch subsidiary to the lead bank. Such move has drawn upon on wanted attention to the bank on the possibility of moving the risk to the Bank Holding Company at book value for the opportunity of FDIC coverage. Click here for the Bloomberg article about this.

Although many large institutions have done this move in the past, the question of timing comes to light on why now. I’m sure many investors such as Warren Buffet and the like might want to know as well. In my opinion BOA being a 2nd largest bank by asset size in the United States I would highly doubt the FDIC would want to exposed to such a failure. However, there have been calls in place both on youtube and other social media to make a run on the bank in November 5th and December 7th of this year. Here is the original article from Reuters and below the 6 month stock price chart for BOA.

Source: http://www.reuters.com/article/2011/10/19/idUS200361147020111019